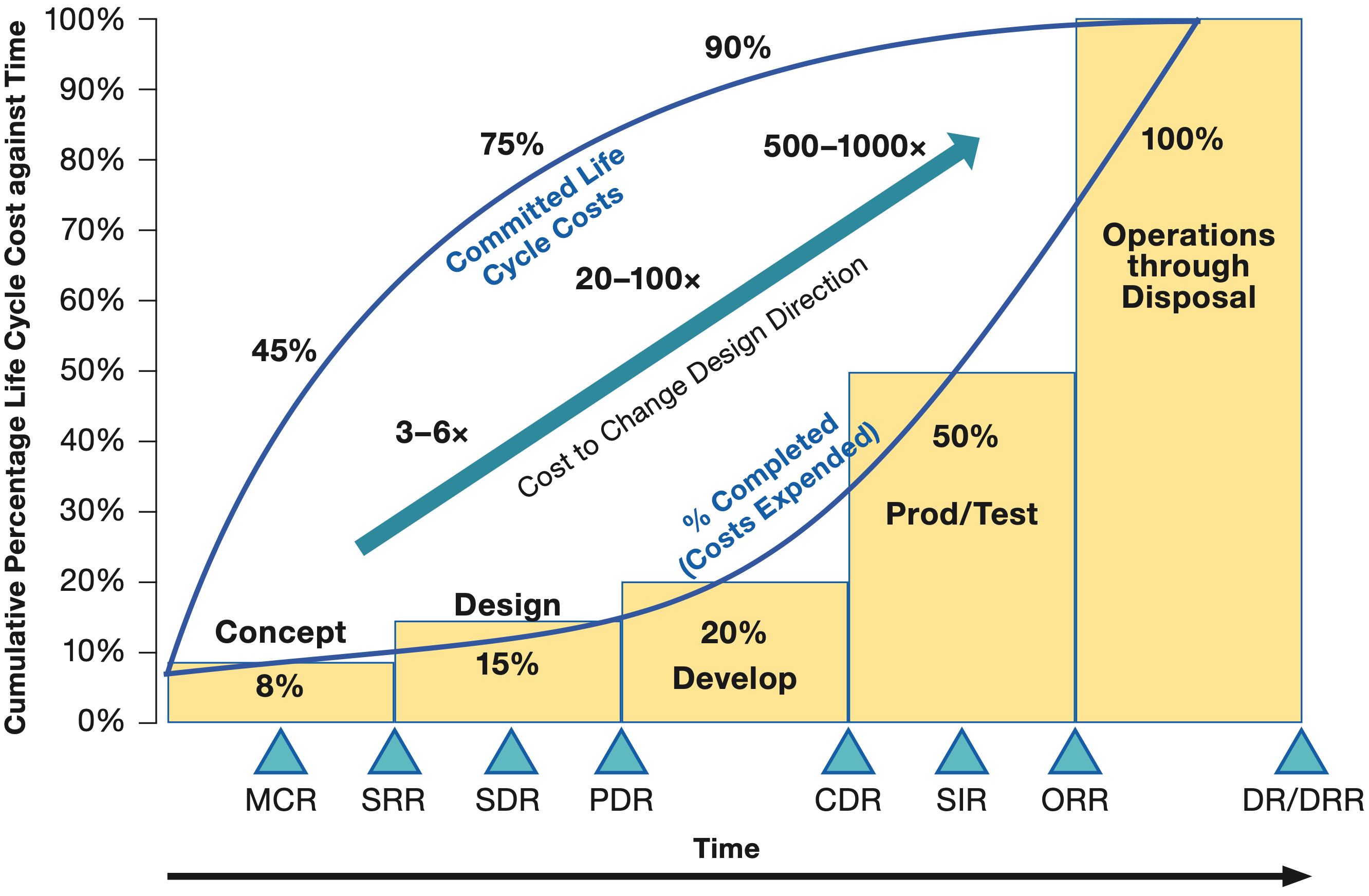

My grandmother – or maybe it was a college professor – frequently reminded me that the longer we wait to fix a problem, the more it costs. Leave it to the engineers at NASA to put this adage into a chart and calculate just how much more it costs based on how long we wait. Their ‘Life-Cycle Cost Impacts from Early Phase Decision-Making’ chart (shown below) suggests BaaS banks battling regulatory enforcement face expenses 500-1000x more than a new entrant.

Life-cycle cost impacts from early phase decision-making

Source: NASA Systems Engineering Handbook

The BaaS bank translation

How do we get from their chart with NASA-specific review acronyms and life-cycle stages to saying incumbent BaaS banks have a real problem?

First, take the “Concept” stage on the far left of the chart and consider this to be when a prudent BaaS bank is first considering the market opportunity. This is before they onboard a partner. Before they sign up with a technology intermediary (e.g. Unit, Q2 Helix, Treasury Prime, etc.).

Second, take the “Operations through Disposal” stage on the far right of the chart and consider this to be a BaaS bank that has multiple BaaS partnerships and is in the middle of a second or third regulatory exam with significantly greater expectations.

The blue diagonal arrow with numbers above it (e.g. 3-6x, 20-100x, 500-1000x) is NASA’s generalized estimate of the cost to change the design of any system. The bank’s system is a Risk and Compliance Management System. The chart suggests that existing banks need 500-1000x more investment to modify their existing risk and compliance program to meet the current expectations compared to the new BaaS bank that is just starting its investment.

Yeah, but 500-1000x more?

At first, this seemed a little exaggerated to me. Then, I read another of the seemingly weekly consent orders. The enforcement actions require the setup of a Board Committee ($), independent parties to review the program ($$), lookback reviews ($$$), “recommended” hiring ($$$$), and growth restrictions (in some cases, offboarding programs) even while increasing the costs to operate ($$$$$).

An investment banker covering community banks shared their thesis with me that existing BaaS banks have an insurmountable advantage over new entrants. I’ve heard other bankers rationalize all the reasons why there won’t be many new BaaS banks.

To me, 500-1000x doesn’t seem that far off. New BaaS banks have the benefit of learning from others’ previous mistakes, having a more complete picture of regulatory expectations, no dominant competitors, and they are starting with a clean slate (and not to mention all of the great information on bankingembedded.com). Putting on my old strategy officer hat, being a new BaaS bank looks like a compelling position to be in if you’re willing to make the initial investment and weather the current storm.